SMI: October ad spend recovers, Nov/Dec well above 2019 levels

• Among the key categories, the largest gain this month was from the food/produce/dairy category (+42%)

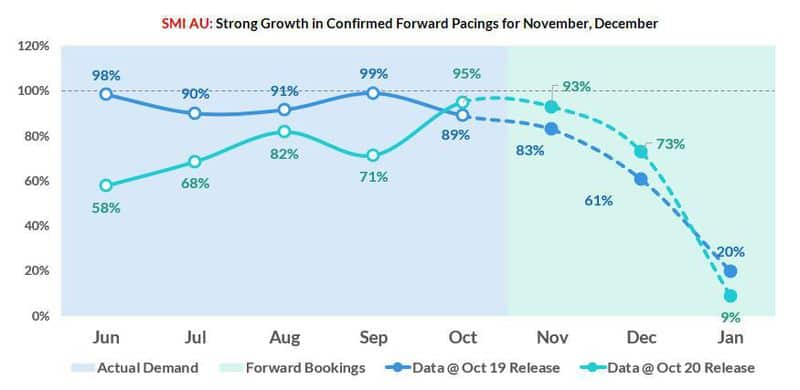

Australia’s media agency market is finally emerging from the Covid crisis, with the latest SMI data showing the market back just 4.8% in October and the forward pacings detail confirming November and December ad demand is well above where it was at the same time last year.

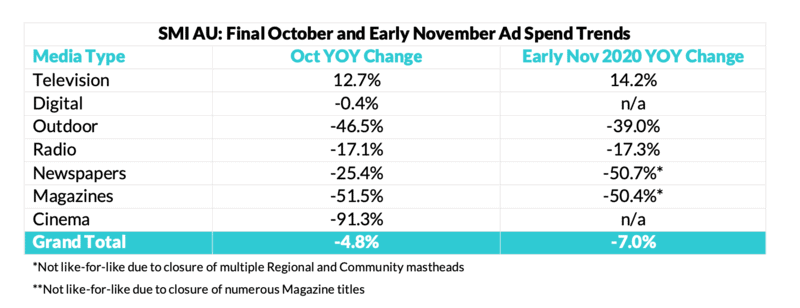

The October market was boosted by the move of the AFL and NRL finals and Grand Finals into the month which resulted in a 12.7% increase in television bookings, with Metropolitan TV ad spend up 15.7% year-on-year.

Digital bookings were stable in the month (-0.4%) mostly due to soaring advertising demand for social media sites (+45.5% in October) with each of Facebook, Snapchat, TikTok, Pinterest, Twitter and LinkedIn all reporting growth of a minimum 34% compared to October 2019.

And SMI AU/NZ managing director Jane Ractliffe said the stronger market demand was continuing, with early November data showing the market so far back 7% with a week’s trading still to come.

“The October SMI data has confirmed the ad market is well and truly leaving the Covid crisis behind, while future demand is also quickly accelerating in both November and December,” she said.

“Our forward pacings data – which compares the current level of confirmed future ad spend to that at the same time last year – shows November advertising demand is already 10 percentage points ahead of where it was in November 2019 and for December the level of confirmed ad demand is now 12 percentage points higher, and that increase in demand is the highest ever seen.”

The leading media trade publication in Australia.

Get our top stories straight to your inbox daily by signing up to our Newsletter

By providing your information, you agree to our Terms of Use and our Privacy Policy. We use vendors that may also process your information to help provide our services.

However, the TV market in November is affected by a few timing issues which aided its early 14.2% increase in ad spend with the month featuring three highly competitive State of Origin matches that were broadcast in June/July last year. But there was also no cricket broadcast this November, but it featured last year.

“The early signs for November are very encouraging and show the market is now on the cusp of returning to growth as there was a week’s trading still to occur when that early November data was collected. We may be reporting our first month of growth in more than two years next month,” Ractliffe said.

Other interesting trends emerging in the October data include an ongoing decline in programmatic ad spend, with premium content sites regaining the position of the third largest digital sector in October, reversing many years of erosion by programmatic ad spend.

The pure play video sites sector (which includes sites such as YouTube and the TV streaming sites) also reported good growth in October ad spend (+15.5%) and within the traditional media regional TV (+8%) and regional radio (-2.7%) were the strongest performers.

Among the key categories, the largest gain this month was from the food/produce/dairy category (+42%) but Covid continues to affect other key verticals with travel ad spend back 76% and the movies/cinema/theme park spend was back 87% year-on-year.

More from Mediaweek

The leading media trade publication in Australia.

Get our top stories straight to your inbox daily by signing up to our Newsletter

By providing your information, you agree to our Terms of Use and our Privacy Policy. We use vendors that may also process your information to help provide our services.