Early SMI data suggests lesser COVID-19 impact on ad demand

• No wipeout: Agencies spend $17m in past two weeks

The Australian and New Zealand media markets are unlikely to report the higher levels of decline in advertising demand often speculated about due to the Coronavirus pandemic, according to early ad spend data from Standard Media Index.

SMI AU/NZ managing director Jane Ractliffe said SMI, which collects the actual advertising payments made by media agencies on behalf of their advertiser clients, organised special advertising data collections in both the AU and NZ markets Tuesday night to provide the first insight into how the Coronavirus has impacted ad demand in the past two weeks.

And while the market has been awash with talk of campaign cancellations, the net impact for Australian agency advertising in the past two weeks has been an inflow of $17 million in agency bookings. But in NZ, which has been more bullish all year with a higher level of future confirmed bookings, SMI is reporting a $7.1 million decline in April bookings.

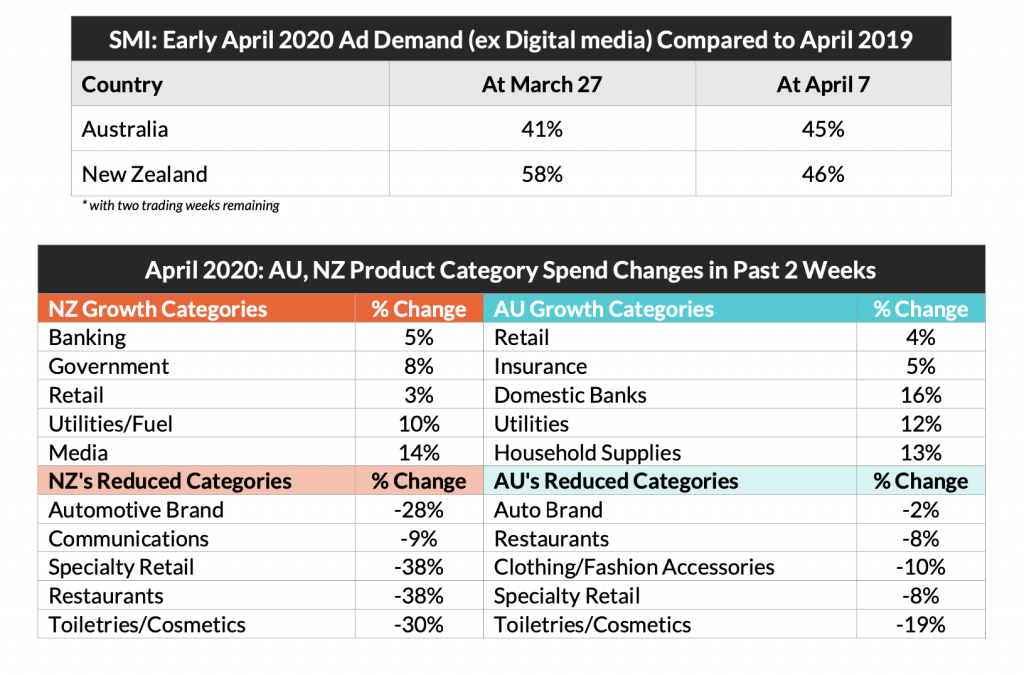

But both markets are now showing similar levels of forward demand in April with the confirmed value of Australian bookings already 46% of that reported in April 2019, and in NZ that figure is 45%. And that’s with more than two weeks of trading still to occur in the month.

“SMI’s actual data shows the market is not experiencing the wipeout some people have suggested,” Ractliffe said. “The market is back, but suggestions of 50- 60% declines will just not happen. Some media are tracking well from an agency perspective and many large product categories have continued to grow their media investment in April,” she said.

“Even if another ad was not bought in the whole of April, the worst case scenario for the AU market is a decline of 55% and 54% for NZ. But of course there’s a mass of paid ads that we’ll see in the next two weeks on our TVs, in our newspapers, on the radio, in magazines, outdoor and on our phones and tablets. Given the amount of ad revenue we’d usually see come through in the next two weeks, the likely decline at worst will be 25% to 30%.

“If media are seeing declines of more than 50%, that will be more due to the devastating impact of evaporating advertising from the small business sector given much of that part of our economy has closed. Media agency demand is not falling anywhere near the same level.”

The leading media trade publication in Australia.

Get our top stories straight to your inbox daily by signing up to our Newsletter

By providing your information, you agree to our Terms of Use and our Privacy Policy. We use vendors that may also process your information to help provide our services.

Ractliffe said TV and newspapers appear to be the early beneficiaries of the recent changes in media plans by agencies on behalf of corporate advertisers.

Australia’s national newspapers are already reporting a 30% increase in agency bookings for March and in the last two weeks agency spend on newspapers has grown 14% for the month of April (the highest percentage increase in Agency spend of any media for the month).

In both countries television is reporting the highest level of future confirmed bookings of any media, with the value of confirmed TV bookings for April already 57% of that achieved last April.

As for the product categories, in the past two weeks SMI is reporting a strong increase in April investment from retailers in both countries (mostly supermarkets), while insurers, domestic bank and utilities have also grown ad spend in both markets since the ‘stay at home’ message came into effect.

SMI is today also releasing the first look at early March data for both markets. In NZ, the market came into the COVID-19 crisis in a strong position with agency demand up 4% in March (ex digital) which also brings its March quarter growth to 4% (ex digital). In Australia, the very early March data shows the market back 11% ex digital.

Ractliffe said SMI would again update the market on ad demand next week with the release of the usual interim March results for Australia and New Zealand and was committed to keeping the market informed during this unprecedented time.

“It’s never been more important to have the facts about how advertising demand is tracking and we want to ensure all our media and advertiser stakeholders continue to have an accurate view of the market on which to make important decisions in this unprecedented time,” Ractliffe said.

More from Mediaweek

The leading media trade publication in Australia.

Get our top stories straight to your inbox daily by signing up to our Newsletter

By providing your information, you agree to our Terms of Use and our Privacy Policy. We use vendors that may also process your information to help provide our services.